Investment: Avoiding the Sirens’ call

How disciplined rebalancing keeps your investments off the rocks

In Greek mythology the Sirens lured sailors with their enchanting music and voices to shipwrecks on the rocky coast of their island. The hero Odysseus survived the Sirens’ call by getting his sailors to plug their ears with beeswax and tie him to the mast.

Evolution has left humans poorly wired to resist the Siren call of the markets to dash our investment dreams on the rocks.

Our emotions are powerful forces that can cause us to buy high and sell low, which is exactly the opposite of what we should do. If this is repeated over a long period of time, it will cause serious damage to our investments and more importantly our financial dreams.

To avoid this fate we need to use similar tactics to Odysseus.

The first and most important tactic is to ignore the news (which these days is more about entertainment than information) and resist the urge to keep checking our investments. This can be bad for our wealth.

But ignoring our investments forever is not a good idea either for two reasons:

The first is emotional. Eventually the urge to “do something” and “take control” can become too great. Inevitably this will be at the wrong time.

The second is that over time if left unchecked the Growth Assets in the investment will grow faster than your Defensive Assets. So the investment will eventually become more risky than is comfortable.

The answer is to agree when to rebalance the investment back to the target investment mix beforehand. Rebalancing whenever the investment strays too far away from the target mix enforces a systematic ‘buy low, sell high’ discipline which enhances the long-term return of the investment.

By lashing ourselves to the rebalancing mast we can stay disciplined and avoid the financial rocks.

Investment: Suck it and see!

How thinking of boiled sweets can put tax in its place

When investors are disappointed by the returns on their investments they often blame their ISA or pension. But it is almost certainly the underlying investments that will be to blame.

An investment can be thought of as having two parts: the tax wrapper and the underlying investment.

The tax wrapper determines how the underlying investments are treated by HM Revenue & Customs. Usually the tax wrapper is designed to protect your money from the clutches of the tax man.

An ISA is an example of a tax wrapper. Money in an ISA grows (largely) free of tax and there is no income or capital gains tax to pay when you take money out.

The money inside the ISA will either be saved in cash or invested in funds. It is the performance of this cash or funds which will decide whether the investor’s experience is a good one or not.

It may help you to think of a boiled sweet which also comes in two parts

The sweet wrapper, which keeps the sweet fresh, is like the tax wrapper which keeps your underlying investment fresh by reducing the tax paid.

The sweet inside, which comes in different flavours, is just like the underlying investment, which comes in different investment types. Just as a sweet can be too sour or too sweet, an investment can be too risky or boring for individual investors.

Tax is not as important as getting the right investment flavour or having low investment costs.

Investment administration systems now make organising your investments in a tax-efficient manner a mere formality.

So remember, concentrate on the flavour not the wrapper!

Investment: Rise above the noise

Can I beat the markets?

The good news is that the investment markets themselves deliver nearly all the returns in your investment. So there is little need to worry about timing your investing in and out of the stock market or picking the best stocks.

Getting your investment philosophy right

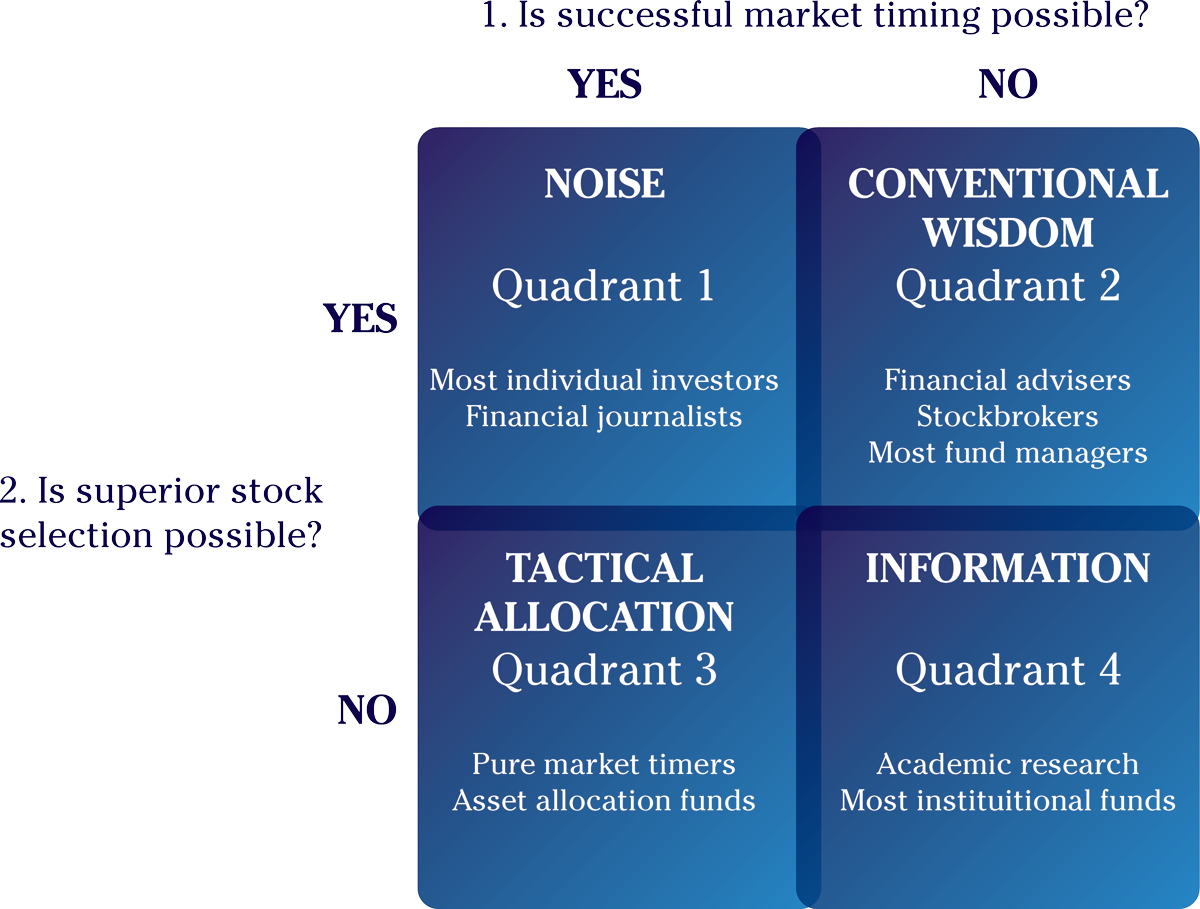

The two most important money management questions are:

- Is successful market timing possible?

- Is superior security selection possible?

Most investors will fit into one of four world views depending on their answers to these questions:

The Quadrant 1 investor expects to both profitably predict the short-term movements of different asset classes and choose securities which will outperform the asset class as a whole. Most individual investors fall into this quadrant with the encouragement of the media.

Quadrant 2 investors (including most investment professionals) know they cannot predict market swings accurately. But they believe it is possible to choose the securities within a particular market that will outperform the market as a whole.

Quadrant 3 investors believe that whilst there is no point selecting individual stocks within an asset class, they can maximise gains by jumping from one asset class to another. The strategies described by Quadrants 1 to 3 are known collectively as active strategies. The reality is these methods fail to even match the market return, particularly after costs and tax over the long term.

The Quadrant 4 investor believes that markets are efficient, and that security prices are moved in the short run by surprises that people cannot foresee. Or at least, markets are efficient enough so the costs of Active money management strategies outweigh any small advantages gained. This is our world view and the one backed up by most academic studies. This world view demands that advisers don’t concentrate on the money, but on the client and their targets and risk profile instead and structure their portfolio accordingly.

Whilst it is not possible to consistently beat the market by timing or picking stocks, the good news is we don’t have to do either to have a successful investment experience. This may be the first time you have been asked to accept that the Quadrant 4 or Passive Asset Class investing is the optimum money management strategy. So let’s look at some of the reasons why Passive Asset Class investing is not as widely accepted as PageRussell believes it should be.

Individual investors

It is a central tenet of western culture that if you work hard enough success will follow. So it is intuitive for people to believe that if they (or their financial adviser) turn over enough stones they will find some gems. The facts are that this is not the case with investing. The main reason for this is the market is not made up of amateurs, but sophisticated professionals. The investment banks now have computers constantly scouring the internet for news and executing trades based on that news within milliseconds. The other reason is that this trading activity costs money, which outweighs any potential gains from the stock picking or market timing.

Humans are driven to want ever more. It is one of the fundamental drivers of human evolution and progress. So it is not surprising that investors are reluctant to accept, ‘just’ the market return and are susceptible to promises (implied or otherwise) of better than market returns. Accepting the Quadrant 4 world view means accepting there is no such thing as a free lunch. The benefit of long-term return of capital markets comes with uncomfortable short-term volatility. This is a harsh reality for most investors to accept; it is no wonder they stick with their hopes.

Investment professionals

Most investment professionals reject the Quadrant 4 view as it threatens their existence.

The financial media

The job of financial journalists is to write exciting stories. The media will always either highlight the latest financial scandal (fear), or feed the notion that you can beat the market (greed). The Quadrant 4 world view is too boring to keep writing about. It would be nice if all our clients came to us already knowing that passive asset class investing is the optimum strategy. But we need the majority of investors to believe they can beat the market. We want them to go on expending the effort, because that creates the market returns we harvest.

The good news

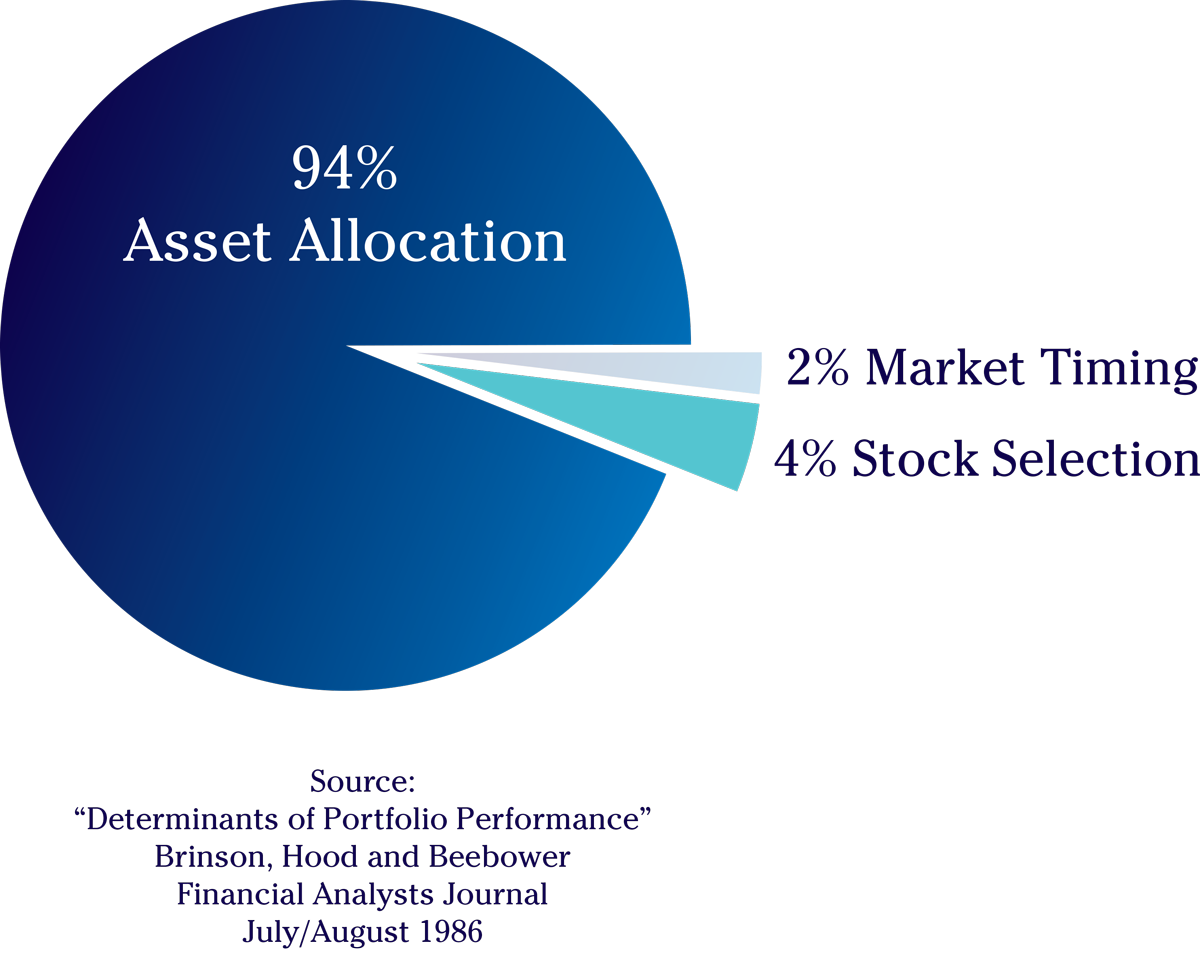

The good news is we don’t have to be market timers or stock pickers to have a successful investment experience. This is because investment mix – or asset allocation – accounts for over 90% of the performance of an investment portfolio.

Investment: Getting the right blend

How much mixer do you like with your spirits?

Investors are faced with bewildering jargon to describe the funds they can invest in. Fortunately, whatever the label on your investment, it will be made up of a mix of the following main investment types:

- Cash,

- Fixed interest (also called bonds),

- Equities (also called company stocks and shares), or

- Commercial property (factories, shops and offices).

It might make sense to think of these different investment types as different flavours. The four investment flavours can be split into two to make things even simpler:

- Growth Assets Equities and commercial property grow faster than inflation over the long term, but their values may go up or down more than you are happy with over the short term. You can think of growth assets as being a bit like neat spirits. It gets you drunk quickly but the side effects are too unpleasant for all but a few.

- Defensive Assets Cash and fixed interest (or bond) returns are lower than those of the growth assets over the long term, but any changes in value are less alarming too. Just like adding a mixer to a spirit, you add defensive assets to make your investment palatable. You should get to the same destination, over a longer time period and without the nasty side effects.

Hershey or Nestlé? – The two approaches to blending your investments

The variables of risk and return drive the two main methods of blending investments. Whilst it is a sweeping generalisation, it’s convenient to label the two approaches as the American or Swiss way. The American way is to concentrate on the risk required and blend the investment to meet that need – no matter what the associated risk is. The Swiss way is to blend the investment based on the risk you prefer and can afford then blend the investment. The down side is that the expected rate of return may not be enough to meet your financial goals.

It is your money

You will have to live with the ups and downs with any investment strategy; therefore PageRussell adopt the Swiss approach. Comfort comes at a price. You may have to do one or more of the following:

- Adapt your goals,

- Save more, or

- Accept more risk.

Having a financial plan makes it possible to work out which combination of strategies is best for you.

Financial planning: Pull the right levers

Money is just a tool to help you live the life you want

At PageRussell we create your financial road map using a personal financial forecast. We do this by quantifying your life goals into a target amount of cash over a timescale. Then we work out how much money is available now. Based on how much money you plan to save and your tolerance to investment risk, we calculate whether or not you are on track to meet your goals.

We make recommendations about how to reduce your investment costs and tax. This means the main levers you can use to achieve your lifestyle targets are:

- Change how much is in the pot, that is by increasing earnings or changing spending.

- Change the mix (or asset allocation) of the investments.

- Change the target amount.

- Change the timescale.

- Insure against risks such as ill health and death.

These are all levers that you control, which is why we think financial planning has to be a collaborative process.

Financial planning: Trick yourself to financial success

How do I stay on track?

Most economists assume we always make calm and rational financial decisions. But real life is messier and we humans are predictably irrational. We put an emotional value on money. Perceived losses hurt more than gains give pleasure; so we avoid risk. We tend to latch onto high numbers, increasing the chance of feeling a loss. We herd together even when it is not in our best interests. It takes super-human powers to stay rational. It is easier to trick yourself to financial success. Here are some nudges you can use to stay on course:

-

Get some perspective

It can be gut-wrenching if you learn your investments have lost more money than you earn in a year. Anger, regret and fear can take over. Has this ruined your retirement plans? Should you switch to cash and wait till it all blows over? To beat inflation, most people who invest for the long-term need to hold a proportion of their wealth in the stock market. These investments WILL drop in value every so often. If you have a financial plan, you should know how far your investments might fall and what the effects would be, so that when the stock market crashes you can stay calm. The real value of a financial planner is having someone who is impartial to contact when life is getting tough and you need a fresh perspective.

-

Forget the Joneses

We’ve all had to listen to someone (usually a man) drone on about a successful money venture (they never talk about failures). These days you don’t have to be face-to-face, as most money bragging is done online. Because humans are social we often find ourselves thinking “Why aren’t I doing that?” or worse “Have I got it all wrong?”Keeping up with the Joneses is bad for you. Mr Jones’ advice is unlikely to be right for you. If you find yourself worrying about what he is doing with his money recite: “I wouldn’t take this man’s medicine, so I won’t use his financial ideas.”

-

Do your fire drill

If you are invested in the stock market you should regularly remind yourself that your investment value WILL go down sometimes. The best way to do this is an investment fire drill. Take the proportion of your investment invested in the stock market, halve it and take that sum away from the total. Then ask yourself how you feel. Be honest. If this loss gives you real concern you should consider reducing the short-term risk in your portfolio.

-

Turn down the noise

Keeping a close eye on your current account to manage your spending is a good idea. Doing the same with your long-term investment is not. It gives you a false sense of control, there is more chance of seeing a loss and this leads you to trade too much. Try to hold the right mix of investments for you in just one fund and look at it only once a year. And turn off your news feed; it is noise not news.

-

Hide or label your cash

If you want to hang on to your money, hide it from your current account. Set the date for your bills on or just after pay day. If you can, make pension or ISA contributions direct from your salary. Make your savings mean something by labelling them with the goals you are saving for. You are less likely to raid your holiday or new house pots to buy new shoes than if you have one large savings account.

-

Think like a pilot

The secret to personal financial success is to do the boring-but-important stuff regularly. Over time it becomes a habit. The best way to do this is review your financial plan yearly. Sailors and pilots get this instinctively. Throughout a journey they go back to the plan, check to see they are on course and adjust accordingly.

Investment: What are risk and return?

“Risk” means different things to different people: danger, uncertainty, opportunity or thrill. In the investment world “risk” or “volatility risk” normally means the amount your investment goes up or down compared to the expected growth rate over time. At PageRussell we often call this “uppy-downiness” because we think it makes more sense.

The decision on how much risk you should take with your investments (your risk budget) depends on:

- How much risk you need to take.

- How much risk you can afford to take.

- How much you prefer to take.

Risk required

The risk you need to take can be calculated as the rate of return – that is the amount you need your investments to grow by – to achieve your financial goals.

Risk capacity

The amount of risk you can afford to take is often called your capacity for loss. An example of capacity for loss would be when you need all the money in 12 months. In this example if the stock market crashed by 20% the odds on you making the money back in time are not great. So it is best not to take the risk in the first place.

Risk tolerance

The risk you prefer to take is often called your risk tolerance. Investment risk tolerance is a relative measure, just like judging temperature. You know what you think is hot or cold, but this will be different to what others think. To agree the temperature we need a thermometer. Advisers who rely only on their own judgement of their clients’ tolerance to investment risk will judge their clients risk tolerance relative to their own. This adviser bias is dangerous. To obtain a more scientific measurement of your investment risk tolerance we use the risk profiling services of Finametrica Corporation. You can try out Finametrica’s technology for yourself at www.myrisktolerance.com.

Financial planning: Supermarket sweep

Traditional financial advice treats you like a supermarket customer

Influenced by traditional financial advisers, most people only buy a financial product as a reaction to a life event. They might move house and buy a mortgage; change jobs and buy a pension; have children and buy life insurance; or they might read in the financial press that gold funds will grow at 20% minimum every year and invest all their money there. This series of uncoordinated events results in a trolley full of plans.

Will you have what you need at the check out?

The problem is there is no form of measurement until it is too late. You reach the check out at retirement and hope that you have enough in your trolley to last you through. Or something goes wrong on the way to the check out (such as an illness or accident) and you have to rummage in the trolley in the hope that there’s something there to deal with the problem.

This retail service is flawed

Even in the best hands financial advice delivered this way will be at best reactive and almost always result in the sale of a product. In the worst hands this service can lead to biased and expensive advice; with no measurement of how far the existing arrangements will get you towards your objectives.

Advice not products

Because you are buying policies, the people who deliver the traditional advice service to you tend to get paid according to what they sell. This payment method works in most retail environments. But we think most people go to a financial adviser for advice – not a shopping trip.

The alternative is financial planning

A financial planning service is more comprehensive and proactive. It equips you with the tools you need for your financial journey through life. Crucially it measures your progress. Your Financial Plan shows you how much to save or spend; to invest or repay debt; how fast your investment needs to grow, the right investment mix you need to live your desired lifestyle. Very often a financial planning service will recommend you avoid or get rid of financial products. So the service needs to be fee-based to protect your confidence and trust in the impartiality of the service. Please call Tim or Stephen if you would like to know more: 0845 345 6282.

Financial planning: What is wealth?

At first glance this seems like a strange question to ask. Surely the answer is obvious?

But people use a wide variety of measures to keep score of how wealthy they are. For example, some define wealth in terms of how much they can borrow; whilst others keep score in terms of cash in the bank or the house they live in.

At PageRussell we think of a person’s wealth in terms of the number of days they can go without working for a living.

You are financially independent if you have enough assets to pay for your lifestyle without having to work.

This measure of wealth is dependent on your own lifestyle goals and financial targets.

It is why we might think the person riding in the back of the Roll Royce is poor but his chauffeur is rich.

If the Rolls Royce owner has borrowed money to buy the car, house and other assets, but has no savings or investments that can provide an income, he is going to run out of money fast if he has to stop working.

The chauffeur on the other hand may be close to retirement with a pension from another job, a small paid for house and modest investments. But crucially the assets will provide enough income for the life he wants to live. He works only because he wants to. Out of the two men, he is the one who is truly wealthy.

Investment: What is investing?

Investing versus saving and speculating

Investing means different things to different people.

Here at PageRussell we use the word “investing” to describe putting your money away for the long-term in an investment where you can expect a link between the short-term volatility risk taken and the long-term return.

Investing is NOT:

- Putting aside some cash for short-term needs. That is “saving”.

- Putting money in assets which do not provide an income and you do not want to sell to fund your lifestyle. We call these “used” assets.

- Putting your money into something where there is no link between risk and reward. That is “speculating.” Some people call this a “fun fund” or “racing money”. It is OK to knowingly speculate, provided you can afford a 100% loss. The problem is that many unwitting speculators think they are actually investing.